![]()

Want to know about my new book and its upcoming launch events? Sign up here...

![]()

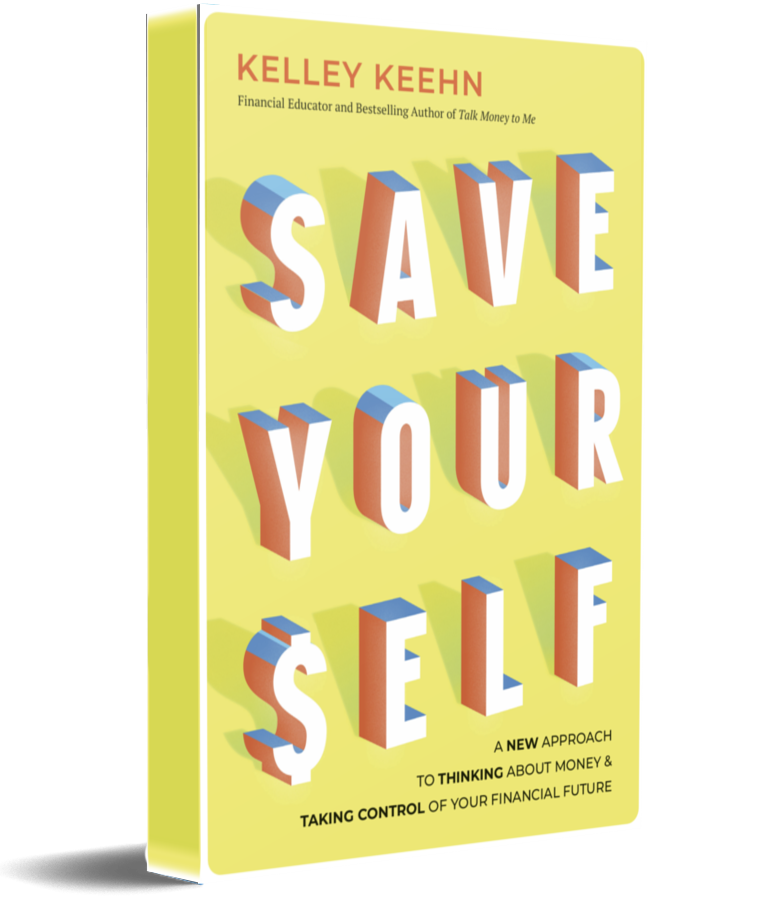

SAVE YOUR SELF

BUY NOW

💰 Save Your Self by Kelley Keehn

Financial Educator and Bestselling Author from Money Wise Institute

In Save Your Self, Kelley Keehn offers a fresh, empowering approach to personal finance — one that’s less about complicated spreadsheets and more about understanding your relationship with money. Drawing on years of experience as a financial educator, Keehn helps readers uncover the habits, beliefs, and blind spots that hold them back from achieving true financial security.

Through relatable stories, practical tools, and clear strategies, you’ll learn how to:

• Take control of your money — without fear or guilt

• Build confidence in financial decision-making

• Save smarter, spend intentionally, and plan for a secure future

• Protect yourself from financial stress and setbacks

Whether you’re just starting out or looking to rebuild, Save Your Self is your guide to thinking differently about money — and taking control of your financial future with clarity, courage, and confidence.

Financial Educator and Bestselling Author from Money Wise Institute

In Save Your Self, Kelley Keehn offers a fresh, empowering approach to personal finance — one that’s less about complicated spreadsheets and more about understanding your relationship with money. Drawing on years of experience as a financial educator, Keehn helps readers uncover the habits, beliefs, and blind spots that hold them back from achieving true financial security.

Through relatable stories, practical tools, and clear strategies, you’ll learn how to:

• Take control of your money — without fear or guilt

• Build confidence in financial decision-making

• Save smarter, spend intentionally, and plan for a secure future

• Protect yourself from financial stress and setbacks

Whether you’re just starting out or looking to rebuild, Save Your Self is your guide to thinking differently about money — and taking control of your financial future with clarity, courage, and confidence.

Rich Girl, Broke Girl

In stores and online now

Do you want to know how to pay off that debt and start saving?

Ready to negotiate a salary raise or better benefits?

Do financial terms and options make your head spin?

Here’s the good news: we as women have more financial freedom and money now than ever before. Here’s the bad news: when it comes to money, many women become paralyzed by financial management and sometimes even defer big decisions to other people, much to their detriment.

What’s the solution? Financial empowerment.

In this handy guide, you will learn how to:

- Discuss money with your partner

- Determine realistic and attainable goals

- Negotiate for the salaries and benefits you deserve

- Splurge occasionally while still saving money

- Understand financial risks and make good investments

- Gain control of your financial destiny

Ready to negotiate a salary raise or better benefits?

Do financial terms and options make your head spin?

Here’s the good news: we as women have more financial freedom and money now than ever before. Here’s the bad news: when it comes to money, many women become paralyzed by financial management and sometimes even defer big decisions to other people, much to their detriment.

What’s the solution? Financial empowerment.

In this handy guide, you will learn how to:

- Discuss money with your partner

- Determine realistic and attainable goals

- Negotiate for the salaries and benefits you deserve

- Splurge occasionally while still saving money

- Understand financial risks and make good investments

- Gain control of your financial destiny

![]()

![]()

![]()

![]()

![]()

Talk Money To Me - COVID Edition

BUY NOW

In this new and updated emergency and pandemic-focused edition, Kelley Keehn tackles how to spend, save, and plan for your future, even in times of economic uncertainty.

You can gain control of your debt, learn to save for your future, have a life, and feel good about money all at the same time. And—spoiler alert—you don’t need a budget to do any of this! You’ll learn:

-How to weather economic uncertainty and make wise financial choices during the pandemic

-How to build good credit (and get rid of bad credit—especially credit card debt)

-What all these dreaded acronyms mean and how they can work for you—TFSA, RRSP, RESP, CFP, CPP, CERB

-How and when to invest for your future

-How to talk about money with your partner—and everyone else in your life

-How to save for a mortgage and then work towards being mortgage-free

-How to have fun, splurge once in a while, and still save money

You can gain control of your debt, learn to save for your future, have a life, and feel good about money all at the same time. And—spoiler alert—you don’t need a budget to do any of this! You’ll learn:

-How to weather economic uncertainty and make wise financial choices during the pandemic

-How to build good credit (and get rid of bad credit—especially credit card debt)

-What all these dreaded acronyms mean and how they can work for you—TFSA, RRSP, RESP, CFP, CPP, CERB

-How and when to invest for your future

-How to talk about money with your partner—and everyone else in your life

-How to save for a mortgage and then work towards being mortgage-free

-How to have fun, splurge once in a while, and still save money

Talk Money To Me

BUY NOW

Catch my newest book, published by Simon and Schuster.

Learn how to save and spend wisely, feel good about money, and start living a more balanced life.

No matter your age, salary, social or relationship status, money is an important part of your life. Yet, somehow, talking about your money situation is hard. Why is it that you know more about what goes on in your friend’s bedroom than with their bank account? Do you know if your parents have a will or if they’ll leave a legacy? How many of your colleagues are still paying off student debt but are jet-setting around the globe on multiple credit cards?

Learn how to save and spend wisely, feel good about money, and start living a more balanced life.

No matter your age, salary, social or relationship status, money is an important part of your life. Yet, somehow, talking about your money situation is hard. Why is it that you know more about what goes on in your friend’s bedroom than with their bank account? Do you know if your parents have a will or if they’ll leave a legacy? How many of your colleagues are still paying off student debt but are jet-setting around the globe on multiple credit cards?

Protecting You and Your Money:

ORDER NOW

In 2016, over 4 billion records were stolen globally. And according to a new CPA Canada survey, nearly one in three people have been victims of financial fraud. This book will help you to: protect yourself by preventing fraud, spot current scams and avoid them, recapture your life if your identity has been stolen, and learn where to find where to go for help and support. Protecting You and Your Money; A Guide to Avoiding Identity Theft and Fraud was technically reviewed by Jennifer Fiddian-Green, Fraud Investigations Partner, Grant Thornton LLP.

A Canadian's Guide to Money-Smart Living:

ORDER NOW

Did you know that more than 50% of Canadians are just $200 away from not being able to pay their bills? And, for every dollar of disposable income we bring in, we owe $1.17? Many of us feel that managing money and our financial future is hard work and out of our control, which often leads to us ignoring the issue or putting it off for another day, week or year. Simple everyday solutions are available. They start with learning the basics, being comfortable with the topic of money in the household and finally, asking a financial expert the right questions. A Canadian’s Guide to Money-Smart Living will help you understand how to live money-smart and provide you with step-by-step instructions on how to take control of your financial future.

The Money Book For Everyone Else:

Order Now

Canadians owe nearly $2 trillion dollars in consumer debt and 1 in 5 Canadians couldn’t make it one week without going into debt to pay their bills if they lost their primary source of income. If you want to be financially free, something has to change. It starts with this book! The Money Book for Everyone Else is a guide that will teach you: • How only paying what your credit card company requests might leave you burdened with a balance for decades. • How to protect your financial identity and how failing to do so could result in a life-long nightmare. • How to spot and avoid investment scams. • Why certain credit cards could leave you hungry and thirsty on your next flight. • Navigating the world of Canadian tax shelters, along with the basics of investing and debt. • How to repair and maintain your credit score. • Simple tips for being debt-free sooner. • Questions, criteria, and biases you need to be aware of when choosing your financial team. Written in a simple, straightforward style and loaded with lots of real-world examples and stories for Canadians, this book has everything an individual needs to know to become financially savvy. This is not an advanced guide; specific niche topics such as retirement planning, estate planning, and taxation will only be covered as an overview. There are few interactions that will last throughout your entire life, but your relationship with money is one of them.

She Inc.

ORDER NOW

Experts estimate that you will change not only your job, but your career an average of four to five times in your life. Stability and job security are things of the past. Whether you’re an employee, business owner, entrepreneur, or re-entering the work force, this book is for you! Corporate downsizing, whirlwind swings in the markets, job outsourcing—there has never been a more important time for women to take a proactive approach to their career tracks. Author Kelley Keehn meticulously guides the reader through the paradigm shift of seeing oneself as a corporation. This book offers you, the reader, powerful new insights on how to dramatically increase effectiveness and fast track whatever career path you’ve chosen. With real case studies, you’ll learn how becoming the CEO of your own personal corporation will revolutionize your personal and professional life. As a soon-to-be financially savvy woman, your corporation would not be complete without working capital and cash flow. This book delves into the relevant and essential financial information that you need to know. Chock full of tips, examples, exercises and timely information, She Inc. is a must have for any woman to empower and fortify herself in this ever changing economic environment.

The Prosperity Factor For Kids:

ORDER NOW

Parents need to teach their kids about money, and this book will help! It is divided by age group, from five-year-olds using a piggy bank to teenagers preparing to leave home for the first time. Inside you will find many exercises, examples, and tips to help parents and children become financially fit. It also informs parents about programs and financial products available to children. Learning about money and finance can be both easy and fun. In this book, you will find all of the tools necessary to lay the foundation for the financial health and well-being of your child — the impact of which can't be measured in figures alone.

Praise for The Prosperity Factor for Kids 'Solid, real-world advice that will help parents raise financially savvy and successful kids.' — Rob Carrick, Globe and Mail

Praise for The Prosperity Factor for Kids 'Solid, real-world advice that will help parents raise financially savvy and successful kids.' — Rob Carrick, Globe and Mail

The Woman's Guide to Money:

ORDER NOW

The Woman's Guide to Money helps women take life-changing actions that will free our lives of money-related guilt and worry. By rethinking the way we look at money, we can learn how to help ourselves overcome the barriers that prevent us from pursuing our own prosperity. Many of us tend to have a preprogrammed sense of guilt when it comes to money, when instead we should have confidence and satisfaction.

In this step-by-step guide, women will learn how to see the differences between 'net worth' and 'self-worth,' how to overcome the fear of finances, and how to set goals and follow through with a plan. This book is about freedom, independence, and empowerment; it reveals how women can and should look beyond mere dollars to formulate an understanding of true wealth and abundance -- one that is not about greed and power, but concerned with life-enriching prosperity.

In this step-by-step guide, women will learn how to see the differences between 'net worth' and 'self-worth,' how to overcome the fear of finances, and how to set goals and follow through with a plan. This book is about freedom, independence, and empowerment; it reveals how women can and should look beyond mere dollars to formulate an understanding of true wealth and abundance -- one that is not about greed and power, but concerned with life-enriching prosperity.

Kelley’s other books are currently out of print